🗓️

Mar 30, 2026

Bifurcated Analysis in Mixed-Use Properties

Mixed-use properties are often quoted using a blended cap rate. This presents the asset as a single pricing outcome, even though different components are rarely evaluated that way beneath the surface.

In practice, different uses within the same property, whether multifamily, retail, or office, carry different income stability, lease structures, and risk profiles. When those differences are material, a single cap rate can obscure how risk is actually distributed within the asset. This is where a bifurcated analysis becomes relevant.

How Bifurcated Analysis Works

A bifurcated analysis separates the property into individual components, values each independently, and then recombines the results.

At a high level:

segment NOI by use (multifamily, retail, office, etc.)

apply market-appropriate cap rate to each component

aggregate the values

The goal is not to complicate the valuation, but to reflect how the market prices different risk profiles within the same asset. Notably, the blended cap rate is not an input – it is simply the weighted output of these underlying assumptions.

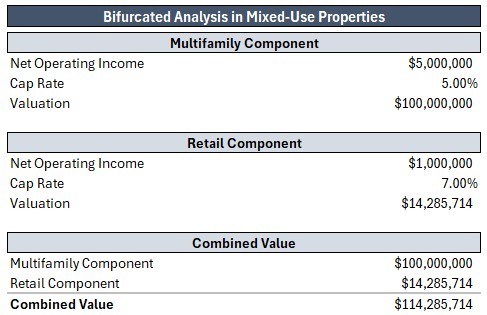

Example

Consider a mixed-use property with the following income streams:

Multifamily NOI: $5 million

Retail NOI: $1 million

Total NOI: $6 million

Using a bifurcated approach:

Multifamily: $5 million at a 5.0% cap rate = $100 million

Retail: $1 million at a 7.0% cap rate = $14.3 million

Combined value: $114.3 million

This illustrates how value is driven by each component’s risk profile, rather than a single blended assumption across the asset.

Where the Blended Approach Works

If there are strong mixed-use comps with consistent pricing, the market may already be capturing these dynamics. In those cases, bifurcation can serve as a supplemental check rather than the primary valuation method.

A blended cap rate works best when:

components are similar in risk

there are strong comparable sales

income streams behave consistently

It becomes less reliable when:

one component carries disproportionate risk

lease structures differ significantly (e.g. short-term retail vs stabilized multifamily)

certain uses are non-core or harder to finance

comparable sales are limited or inconsistent

The Capital Perspective

From a capital perspective, mixed-use assets are rarely evaluated as a single risk profile. Lenders and investors typically underwrite each component based on its own characteristics.

Key considerations include:

which income stream drives repayment visibility

how each component performs under stress

which uses are considered core vs non-core

how risk migrates across components if performance deteriorates

In many cases, capital effectively anchors to the most stable component (for example, multifamily) while applying more conservative assumptions to the rest. This means the non-core component can disproportionately influence the structure of the deal, even if it represents a smaller portion of total income.

This can directly impact:

loan sizing

leverage levels

refinance assumptions

overall structure feasibility

A blended cap rate tells you what the asset trades for. A bifurcated analysis helps explain what’s driving that price and how each income stream is evaluated. More importantly, it provides visibility into where risk sits, what constrains leverage, and how capital will ultimately structure the deal.