How Developers Determine Land Price – Land Residual Analysis

When underwriting development deals, developers typically don’t start with the land price. They start with feasibility.

Land value is often derived through a land residual analysis, which basically solves for what remains after accounting for development costs and required returns. Here, the land price is not an input but an output of the business plan.

It answers the question: “How much can I pay for the land and still achieve my target returns?”

What Drives the Residual

The residual is determined only after modeling the full economics of the project, including:

Builder lot pricing

Horizontal development costs

Impact fees and off-site infrastructure

Financing costs and carry

Required developer return

Only after these variables are solved does the maximum supportable land basis emerge. Land is what’s left over once all other obligations, including profit, are satisfied.

Example

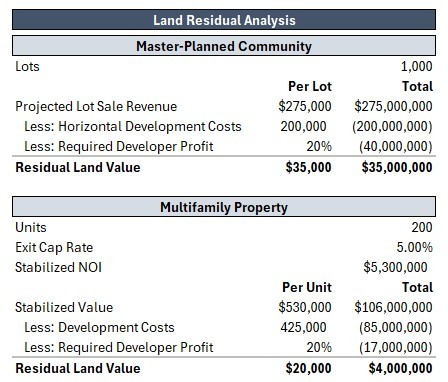

A developer is evaluating a master-planned community with 1,000 finished lots.

Key assumptions:

Average builder takedown price: $275,000 per lot

Total projected lot sale revenue: $275 million

Horizontal development costs: $200 million

Required developer profit: $40 million (20% on costs)

This implies approximately $35,000 per lot as the highest price the project can support while preserving target returns. If land trades above that level, projected returns compress. If acquired below it, developer margin expands. Feasibility determines land value, not comparable sales alone.

Sensitivity and Structural Risk

Residual land value is highly sensitive to assumptions. Small changes in pricing, cost, or return requirements can materially shift what a developer can afford to pay.

For example:

A modest decline in builder pricing reduces the supportable land basis

Unexpected cost inflation compresses developer profit first

Higher return targets lower the maximum land price that can be justified

In some cases, the residual calculation can turn negative. When that happens, the development assumptions do not support the project economics – even if the land were acquired at zero cost. That’s not a negotiation issue; it’s a structural feasibility signal.

Framework Extends to Other Asset Types

The residual land analysis isn’t limited to horizontal land development. The same logic applies across asset types. In multifamily development, for example, the difference is that the developer would start with a project stabilized NOI and apply an exit cap rate to estimate value. After subtracting construction costs, financing, and required returns, the remaining amount represents the maximum land price that supports feasibility. While the inputs differ slightly, the economic logic is the same.

Why Capital Providers Care

The residual analysis isn’t just a developer exercise; lenders and equity investors underwrite the same math when evaluating structural cushion. If land is acquired at an inflated basis relative to projected value, downside protection erodes. If development costs rise or exit assumptions soften, developer profit is the first layer to compress, and risk migrates upward into the capital stack. Essentially, overpaying for the land reduces the margin of safety in a deal, which increases how quickly capital becomes exposed when assumptions change.

Land doesn’t have a fixed value. It has an allowable price determined by the economics of the project. Understanding that distinction fundamentally changes how development risk is evaluated.